Madeleine's Fund: Leaving No Stone Unturned Limited - Forensic examination of the fund accounts by Enid O'Dowd FCA

The Complete Mystery of Madeleine McCann™ :: Professional and Featured blogs :: Featured professional blogs

Page 1 of 1 • Share

Madeleine's Fund: Leaving No Stone Unturned Limited - Forensic examination of the fund accounts by Enid O'Dowd FCA

Madeleine's Fund: Leaving No Stone Unturned Limited - Forensic examination of the fund accounts by Enid O'Dowd FCA

![]() by Guest 11.01.23 19:44

by Guest 11.01.23 19:44

A review of the background to setting up the limited company Madeleine's Fund: Leaving No Stone Unturned and a forensic examination of the company accounts

by Enid O'Dowd FCA

The case of missing Madeleine McCann is unlike any other missing person case. Her parents Kate and Gerry McCann set up a limited company (Madeleine's Fund) less than two weeks after she went missing, and engaged many, mainly legal, professionals, to further their search for her.

This article looks at the history of the Fund, what the audited accounts reveal and the professionals engaged, using material from the book Madeleine and from independent sources.

Madeleine was reported missing by her parents Kate and Gerry McCann on the evening of Thursday May 3, 2007. On 15 May, just 11 full days later, the limited company Madeleine's Fund: leaving No Stone Unturned was incorporated.

The sad truth is that such Funds, Foundations or whatever one chooses to call them are normally set up after a tragic event as a tribute to the person's memory. Amy Winehouse's father has set up a Foundation to provide support and counselling to those seeking help with drink and drug addictions. In October 2002 at the memorial service of murdered teenager Milly Dowler, her parents announced Milly's Fund. This fund was later subsumed into the Suzy Lamplugh Trust set up in 1986 by the parents of missing estate agent Suzy Lamplugh, whose body has never been found. In 2003, Australian teenager Daniel Morcombe went missing. Two years later, his parents set up a Foundation to continue the search and to educate the public. Daniel's remains were found late last year and a man has been charged with his murder.

The book informs us that the limited company arose out of an offer to help 'from a paralegal based in Leicester, via a colleague of Gerry's.' This man worked for the International Family Law Group (IFLG), a firm based in central London.

Kate says 'it was difficult to know what they could do (and anyone in her position would agree) but we decided it would be worth meeting them to discuss the possibilities.' The paralegal accompanied by an unnamed barrister flew to Portugal on the afternoon of Friday May 11. They met that day and had two further sessions with the lawyers over the course of the weekend.

We are told that the barrister, having inspected the proximity of the Tapas bar to their holiday apartment, assured them that their behaviour (in making periodic checks on their children) could not be deemed negligent and was 'well within the bounds of reasonable parenting.' The lawyers also advised about applying to have Madeleine made a ward of court, such status being helpful as the 'courts could make orders to reveal information not otherwise available that might be relevant in our case.'

In the context of the financial help that was then being offered, Kate says the IFLG paralegal advised them to set up a 'fighting fund'. The IFLG would devise the objectives of the fund and instruct a leading charity law firm Bates Wells Braithwaite (BWB) to draw up Articles of Association. The use of the term 'fighting' is odd. Who were the McCanns fighting? Whether 'fighting' is the paralegal's word or Kate's paraphrase is unclear.

It is perhaps strange that the IFLG paralegal, expert in the complex area of international family abductions, would promote the idea of setting up a limited company so convincingly that the McCanns agreed. At the time of the first meeting between the McCanns and the two legal visitors, Madeleine had been missing for only one week.

And, most significantly, Kate says on p.296 of Chapter 19 entitled 'Action on three fronts' writing about the time period autumn 2007, 'gradually my outlook was growing more positive and I was beginning to get past my early certainty that Madeleine must have been taken by a paedophile and murdered.'

If Kate believed that her daughter had been murdered at the time of meeting the legal pair, why would she agree to setting up a Fund to find Madeleine?

Further, in Chapter 19 she tells us, 'by October...we were able to concentrate on our top priority: finding Madeleine...so far beyond following up the odd piece of information outside Portugal, we had not gone down this road...we had been reassured that after a shaky start, the police were doing everything that could be done.'

So if the Fund, set up in record time and presumably at considerable expense, was to find Madeleine, why did it, as Kate herself tells us, do very little for the first four months of its existence other than to collect money and follow up the odd piece of information outside Portugal?

Interestingly the book doesn't mention the names of the paralegal and the barrister who spent the weekend in Portugal to advise them, presumably at their own expense. Her book names and praises other professionals who helped her at different times after her daughter vanished; for example trauma psychologist Alan Pike and Carter-Ruck lawyers Adam Tudor and Isobel Hudson who she says on p.289 'continue to do a vast amount of work for us, most of it without payment, most of it quietly behind the scenes.'

On Sunday May 13 the IFLG issued a press brief release with Ann Thomas, managing partner as the contact person. It merely said that 'last week' they and barrister Michael Nicholls QC had been instructed to act for the McCanns...and that details of how contributions could be made to help get Madeleine back would be made available 'in the next couple of days.'

Presumably then, Mr Nicholls was the barrister who reassured the McCanns about their 'reasonable' parenting. According to the website maintained by his Chambers his principal areas of practice are:

'International and domestic family law and medical ethics, including jurisdiction, recognition and enforcement, conflicts of law, child abduction, international relocation, private children’s cases, contempts, families and the media (freedom of expression and press injunctions) and disputes about medical treatment.'

It is unclear why his particular expertise warranted instruction in a missing child case where there was no issue of family abduction. Apart from his family law experience he also had expertise in media (freedom of expression and press injunctions) but at that time the media was totally supportive of the McCanns.

The press release announcing the appointment of the IFLG contained four names each with a title, one of which was Richard Jones Family Law Executive. Perhaps he is the persuasive paralegal at the Portugal meetings? Mr Jones is not currently included as a staff member of IFLG on their website.

The IFLG was apparently set up not long before Madeleine went missing. The website does not say when. However, since co-founder David Hodson was, according to his website career details working in Sydney until 2005, the IFLG cannot have been founded until 2005 at the earliest.

BWB could not have been contacted before Monday morning May 14 when their offices opened – they had the company incorporated on Tuesday May 15.

A Freedom of Information (FOI) request to the Charity Commission revealed several emails, telephone calls and a telephone conference between BWB and the Charity Commission about the possibility of charity status, for the then unincorporated company, between Monday afternoon May 14 and Tuesday May 15.

BWB emailed Alice Holt, Head of Legal Services (Status and Advice) at 9.39 pm on Monday evening with draft documents for the company as a charity. The email stated there was to be a press launch of the Foundation on Wednesday May 16 and that they awaited instructions on how the founders proposed to operate.

The minutes of the telephone conference held between BWB and the Charity Commission on the morning of Tuesday May 15 record that Alice Holt would look at revising the draft document to a form more acceptable to the Commission. The minutes also record that Commission official Kenneth Dibble was concerned that the press conference set for the next day might send out confused messages to the public unless it was settled what the fund could and could not be used for.

At 1.10 pm on May 15 the Charity Commission received an email from BWB saying their clients were likely to go the ordinary company route rather than pursue charity status. When that email was received Ms Holt was just finalising her promised revisions to the documents submitted to her the previous day. She sent her revised document anyway at 1.28 pm. To meet the Fund launch date of May 16, the McCanns had obviously decided to abandon the apparently hopeful charity negotiations in order to meet the deadline for same day company incorporation. Documents must be filed by 3pm for the company to be incorporated on that day.

It is odd that the McCanns committed themselves to a launch date, set it would appear, before BWB were engaged. In an email to the Charity Commission, BWB refer to being instructed 'this afternoon' (i.e. Monday May 14). What difference would a couple of days delay have made? And it is clear from the documentation that the Charity Commission officials were helpful, and that it was likely that charity status could have been obtained with only minor delay with a little compromise by the McCanns.

Charity status is valuable because it gives an organisation credibility with the public, grant making bodies and local government, making it easier to obtain funds. It also gives the organisation tax advantages. Individuals, sole traders and companies can also benefit from giving to registered charities. Higher rate tax payers may be able to claim a tax refund. Under the Gift Aid scheme a donation is treated as if standard rate tax (20%) has been deducted and this is equivalent to an extra 25p in the £ for the charity. For donations between 6.4.2008 and 5.4.2011 the government gave an extra 3p in the £ supplement. Individuals can also have charitable donations deducted from their salaries, and this is tax efficient as their income tax is calculated on their salary after the donation. See www.hmrc.gov.uk/charities-donors/ for more information on the benefits to an organisation of charity status.

Charities must give an annual report and accounts to the Charity Commission and make these documents available to the public on request. There are also rules relating to fundraising. The trustees (directors) cannot normally receive salary, fees or contracts from the charity and nor can their spouses or other close family members. These requirements are not onerous or unreasonable. Having hired charity experts BWB on the advice of the paralegal, it is surprising that Kate did not let them have a day or two more to explore charity status. And it is surprising that the McCanns have not apparently revisited this issue.

In Chapter 9 in which Kate describes her activities of May 14 she does not mention any dealings with BWB who must have worked very hard that day. Nor does she mention dealing with the paralegal or anyone else at IFLG. There must have been urgent emails and phone calls that day from her advisors. She just states that charity status would not be forthcoming as it was deemed that the 'public benefit' test would not be met, and adds that it (the Fund) 'was set up with great care and due diligence by experts in their field.'

It would be more accurate to state it was set up with great haste and with no apparent reason for that haste.

Rather than going into detail about the busy day she must have had dealing with her lawyers, and why she made the decision to proceed with incorporation and abandon the negotiations for charity status, she talks of going for a run, her first since Madeleine went missing!

She mentions trying to focus on the imminent launch of Madeleine's fund but doesn't say when it was to be or explain why a limited company was required. A press launch can be called at short notice and given the high profile of the case at that time; it would have got a good media turnout however short the notice was. And again, it probably would not have been a problem to get another celebrity at short notice if the one booked to launch the Fund on May 16, Martin Johnson the rugby player, could not meet a rescheduled date.

And after they incorporated the company in 24 hours, BWB applied for British and European trade marks on 18 May 2007 and was given the reference 2456061. These trademarks protected fundraising, internet and print promotions. Again this action was unprecedented at this very early stage in a missing person case.

Review of the Memorandum of Association and Articles of Association filed in May 2007 reveals in 3.1.3 that one of the three objects of the company is to provide support, including financial assistance to Madeleine's family (my italics). Now this could mean uncles, aunts, parents and any blood relations.

This object was not included in the draft submitted to the Charity Commission on May 14. In fact the draft objects were different to the ones actually used for the company as incorporated. The objects in the draft were general, relating to missing persons and the education of the public and the promotion of sound administration of the law. An accompanying note from BWB headed 'proposed activities' did state that initially practically all the donations received would be used for the search for Madeleine, and that substantial funds would not be forthcoming if donations were not restricted in the first instance to her.

The objects of the company as incorporated are specific to Madeleine McCann, with a final object to pursue other cases when the objects relating to her case are fulfilled.

5.2.1 permits payments to directors as beneficiaries and 5.2.4 permits payment of rent where appropriate to directors for premises. Therefore, if the McCanns or family members used a room in their home to work for the Fund, the payment of rent from the Fund would be permitted if they should want it and the Board agreed.

The quorum for Board meetings is one third of the current Board membership. This makes the current quorum two, as there are now six directors. Three directors are family members. The Chairman has a casting vote. John McCann was Chairman until he resigned in July 2010. It is unclear who the current Chairman is. If Brian Kennedy (Kate McCann's uncle) - who was one of the original directors - took over as Chairman, then the McCann family has a majority at board meetings by virtue of the Chairman's casting vote.

The conflict of interest policy (Articles nos 37 and 38) is interesting.

It says (37.1) that directors with a personal interest in an upcoming vote must declare that interest, and (37.2) withdraw from the relevant part of the meeting, and (37.3) not be counted in the quorum for that part of the meeting relating to their personal interest and (37.4) have no vote on the issue affecting them. That is proper governance.

However no 38 states that 'no director shall be regarded as having a conflict of interest solely because he or she is also eligible to receive the support of the Foundation.'

A reasonable person would conclude there is a clear conflict of interest for a family member director if decisions are to be taken on payments of legal fees, rent for part of his/her private house for use as an 'office', and other costs not directly related to the search for Madeleine. The draft documents sent to the Charity Commission only contained no.37 so had those documents been adopted, the McCanns and family members would not have been able to attend or vote on issues regarding certain proposed payments to themselves.

Interestingly a revised Memorandum and Articles of Association was filed in Companies House in December 2011. This deleted the object to provide support including financial assistance to Madeleine's family. This particular object had attracted unfavourable comment in particular from internet bloggers. The motive for deleting this objective more than four years later is unclear. If the Board felt this minority criticism of the object was adversely affecting fundraising, it would presumably have changed it earlier.

On p.138 Kate says there needed to be independent people on the Board as well as John McCann, who is Gerry's brother, and her uncle Brian Kennedy, and at that time she had no idea how important these independent people would be when later there was 'massive scrutiny' of the Fund.

The composition of the Board varied during the first year. At the most there were nine directors meaning the quorum was three. Two were family members; three were friends – Esther McVey, Jon Corner and Dr Peter Hubner. It is not known whether Michael Linnett, a retired accountant based in Leicester or P J Tomlinson (who resigned on 28.12.2007) were friends of the McCanns. Friends can of course be very independent, but the optics of having a majority of family and friends on the Board is not desirable. Gerry and Kate became directors on November 12, 2008. Board numbers were reduced to six, following the resignations of Dr Hubner, Dr Skehan and John McCann in 2010.

Returning to the decision to set up a limited company, nowhere does Kate mention the more logical option of dealing with the donations coming in – to open a new bank account in Madeleine's name, or in the joint names of Madeleine and herself. Such an account could, if desired, have two signatures, her own and an independent signatory such as a solicitor or an accountant.

This could have been done quickly at no cost. Down the line, when the situation was clearer, another structure could have been considered.

In fact it is likely there already was a deposit account in Madeleine's name as many parents open up an account in their child's name as a place for depositing gifts from family and friends, and later to encourage the saving of pocket money. In addition, the Child Trust Fund scheme, introduced in September 2002 by the government and which provided a small amount to kick start these special accounts, could also mean there was an existing bank account in Madeleine's name.

Perhaps, the McCanns, who at the time of the meetings with the lawyers, must have been very distressed, meekly accepted the advice of the persuasive paralegal, and gave him the go-ahead. But the McCanns are clearly intelligent professionals and even given the sad situation, it is hard to understand why they accepted the advice.

The cost of getting a top legal firm to set up a limited company would surely have been of concern to them as the donations coming in were for finding Madeleine and not for lawyers. The legal pair would presumably have informed them of the ongoing compliance costs of operating a limited company such as the audit fee. The audit fees for the four years for which accounts are available total £31,585. You would have expected some comment from Kate in Chapter 9 after the lawyers had left, wondering if she was doing the right thing in spending the public's donations to set up a limited company.

The money already coming in would have been in cash, or cheques made out to the McCanns so there would have been no problem using the money to fund the search. By May 17 a bank account in the company name was open and, most surprisingly, auditors to the company had been appointed.

The Charity Commission in its FOI reply supplied a printout of the official Madeleine website (http://www.findmadeleine.com/) at 17 May 2007 giving information on the Fund including auditor details. Now the directors of a company appoint the auditors. At that date there were three directors, two family members John McCann and Brian Kennedy, and Gerry McCann's immediate boss Dr Doug Skehan. It is quite possible that IFLG or BWB recommended these auditors to the directors but that does not explain the rush to appoint them. It is normal for a company to meet with proposed auditors to agree exactly what they are to do (sometimes auditors may provide other services to the company), to agree fees and to draw up a letter of engagement. It is very unlikely in the time that any meeting with the auditors took place. The first meeting of the board according to Kate was due sometime in the week beginning May 20 which would appear to be the earliest time this non urgent matter could have been discussed.

The auditors appointed were haysmacintyre in London WC1, a 24 partner firm with 150 staff. It is perhaps surprising that the McCanns did not choose a local firm. It is usually more convenient to have a local firm and can be cheaper as a local firm normally has lower overheads than a central London firm. Keeping audit costs down means more money for the search so even though the firm haysmacintyre was possibly highly recommended by the lawyers, one would have thought that this decision did not need to be rushed. Auditing the accounts of a company like Madeleine's Fund would not particularly challenge any qualified person, so there would be no need to take on a large firm with special expertise.

Kate does not mention this firm in the book or the reason why they were chosen and why so quickly. Many new companies would not appoint auditors until later in the financial year though it is good practice to appoint at an early stage to have advice on setting up accounting systems with proper internal controls. But two days after incorporation is fast by any criteria. If an existing business decided to change its status to that of limited company then the accountants to the unincorporated business would normally become auditors to the limited company and would probably have set it up as part of their role. But this wasn’t the case here.

The official Madeleine McCann website says in the section about the Madeleine Fund:

'The majority of the fund money has been and continues to be spent on investigative work to help find Madeleine. Additionally money continues to be spent on the wider awareness campaign – reminding people that Madeleine is still missing and to remain vigilant. None of the directors have taken any money from the fund as remuneration.

Anyone who wishes further information with regards to the financial details of Madeleine's Fund and its professional advisors please refer to the accounts filed at Companies House.'

Kate says of the company on p.138 that 'from the outset everyone agreed that, despite the costs involved, it must be run to the highest standards of transparency.'

Fine words but the reality is different.

Looking at the information provided by the audited accounts as the website advises is interesting, but frustrating in the case of the years to March 31 2009, March 31 2010 and March 31 2011. The first accounts were made up from incorporation May 15 2007 to March 31 2008 and show an operating surplus of £1,031,065.

A page of analysis of expenditure was filed for the accounts to March 2008 which is not a statutory requirement but is good practice for such a company which is a 'not for profit company' according to the official website http://www.findmadeleine.com/.

I put the following question to the Press office at HMRC (Her Majesty Revenue & Customs)

'Has the term 'not for profit' any statutory meaning? It seems to be a catch all phrase used by organisations that may (or may not!) have very worthy aims and objectives.'

And the reply –

'It has no meaning for HMRC, only charities and CASCs (Community Amateur Sports Clubs) benefit from tax beneficial arrangements.'

So this term 'not for profit' which is widely used by companies/organisations that are not normal trading companies has no meaning for the UK tax authorities. While the term is generally used with no intention to mislead, it clearly is a term that should not automatically be taken at face value.

The additional page of expenditure information raised more questions than it answered. I put the questions and comments below to auditors haysmacintyre. When I raised these issues with the auditors, the March 2011 accounts were not yet available and hence the questions only relate to the accounts for 2008, 2009 and 2010.

To continue ...

by Enid O'Dowd FCA

The case of missing Madeleine McCann is unlike any other missing person case. Her parents Kate and Gerry McCann set up a limited company (Madeleine's Fund) less than two weeks after she went missing, and engaged many, mainly legal, professionals, to further their search for her.

This article looks at the history of the Fund, what the audited accounts reveal and the professionals engaged, using material from the book Madeleine and from independent sources.

Madeleine was reported missing by her parents Kate and Gerry McCann on the evening of Thursday May 3, 2007. On 15 May, just 11 full days later, the limited company Madeleine's Fund: leaving No Stone Unturned was incorporated.

The sad truth is that such Funds, Foundations or whatever one chooses to call them are normally set up after a tragic event as a tribute to the person's memory. Amy Winehouse's father has set up a Foundation to provide support and counselling to those seeking help with drink and drug addictions. In October 2002 at the memorial service of murdered teenager Milly Dowler, her parents announced Milly's Fund. This fund was later subsumed into the Suzy Lamplugh Trust set up in 1986 by the parents of missing estate agent Suzy Lamplugh, whose body has never been found. In 2003, Australian teenager Daniel Morcombe went missing. Two years later, his parents set up a Foundation to continue the search and to educate the public. Daniel's remains were found late last year and a man has been charged with his murder.

The book informs us that the limited company arose out of an offer to help 'from a paralegal based in Leicester, via a colleague of Gerry's.' This man worked for the International Family Law Group (IFLG), a firm based in central London.

Kate says 'it was difficult to know what they could do (and anyone in her position would agree) but we decided it would be worth meeting them to discuss the possibilities.' The paralegal accompanied by an unnamed barrister flew to Portugal on the afternoon of Friday May 11. They met that day and had two further sessions with the lawyers over the course of the weekend.

We are told that the barrister, having inspected the proximity of the Tapas bar to their holiday apartment, assured them that their behaviour (in making periodic checks on their children) could not be deemed negligent and was 'well within the bounds of reasonable parenting.' The lawyers also advised about applying to have Madeleine made a ward of court, such status being helpful as the 'courts could make orders to reveal information not otherwise available that might be relevant in our case.'

In the context of the financial help that was then being offered, Kate says the IFLG paralegal advised them to set up a 'fighting fund'. The IFLG would devise the objectives of the fund and instruct a leading charity law firm Bates Wells Braithwaite (BWB) to draw up Articles of Association. The use of the term 'fighting' is odd. Who were the McCanns fighting? Whether 'fighting' is the paralegal's word or Kate's paraphrase is unclear.

It is perhaps strange that the IFLG paralegal, expert in the complex area of international family abductions, would promote the idea of setting up a limited company so convincingly that the McCanns agreed. At the time of the first meeting between the McCanns and the two legal visitors, Madeleine had been missing for only one week.

And, most significantly, Kate says on p.296 of Chapter 19 entitled 'Action on three fronts' writing about the time period autumn 2007, 'gradually my outlook was growing more positive and I was beginning to get past my early certainty that Madeleine must have been taken by a paedophile and murdered.'

If Kate believed that her daughter had been murdered at the time of meeting the legal pair, why would she agree to setting up a Fund to find Madeleine?

Further, in Chapter 19 she tells us, 'by October...we were able to concentrate on our top priority: finding Madeleine...so far beyond following up the odd piece of information outside Portugal, we had not gone down this road...we had been reassured that after a shaky start, the police were doing everything that could be done.'

So if the Fund, set up in record time and presumably at considerable expense, was to find Madeleine, why did it, as Kate herself tells us, do very little for the first four months of its existence other than to collect money and follow up the odd piece of information outside Portugal?

Interestingly the book doesn't mention the names of the paralegal and the barrister who spent the weekend in Portugal to advise them, presumably at their own expense. Her book names and praises other professionals who helped her at different times after her daughter vanished; for example trauma psychologist Alan Pike and Carter-Ruck lawyers Adam Tudor and Isobel Hudson who she says on p.289 'continue to do a vast amount of work for us, most of it without payment, most of it quietly behind the scenes.'

On Sunday May 13 the IFLG issued a press brief release with Ann Thomas, managing partner as the contact person. It merely said that 'last week' they and barrister Michael Nicholls QC had been instructed to act for the McCanns...and that details of how contributions could be made to help get Madeleine back would be made available 'in the next couple of days.'

Presumably then, Mr Nicholls was the barrister who reassured the McCanns about their 'reasonable' parenting. According to the website maintained by his Chambers his principal areas of practice are:

'International and domestic family law and medical ethics, including jurisdiction, recognition and enforcement, conflicts of law, child abduction, international relocation, private children’s cases, contempts, families and the media (freedom of expression and press injunctions) and disputes about medical treatment.'

It is unclear why his particular expertise warranted instruction in a missing child case where there was no issue of family abduction. Apart from his family law experience he also had expertise in media (freedom of expression and press injunctions) but at that time the media was totally supportive of the McCanns.

The press release announcing the appointment of the IFLG contained four names each with a title, one of which was Richard Jones Family Law Executive. Perhaps he is the persuasive paralegal at the Portugal meetings? Mr Jones is not currently included as a staff member of IFLG on their website.

The IFLG was apparently set up not long before Madeleine went missing. The website does not say when. However, since co-founder David Hodson was, according to his website career details working in Sydney until 2005, the IFLG cannot have been founded until 2005 at the earliest.

BWB could not have been contacted before Monday morning May 14 when their offices opened – they had the company incorporated on Tuesday May 15.

A Freedom of Information (FOI) request to the Charity Commission revealed several emails, telephone calls and a telephone conference between BWB and the Charity Commission about the possibility of charity status, for the then unincorporated company, between Monday afternoon May 14 and Tuesday May 15.

BWB emailed Alice Holt, Head of Legal Services (Status and Advice) at 9.39 pm on Monday evening with draft documents for the company as a charity. The email stated there was to be a press launch of the Foundation on Wednesday May 16 and that they awaited instructions on how the founders proposed to operate.

The minutes of the telephone conference held between BWB and the Charity Commission on the morning of Tuesday May 15 record that Alice Holt would look at revising the draft document to a form more acceptable to the Commission. The minutes also record that Commission official Kenneth Dibble was concerned that the press conference set for the next day might send out confused messages to the public unless it was settled what the fund could and could not be used for.

At 1.10 pm on May 15 the Charity Commission received an email from BWB saying their clients were likely to go the ordinary company route rather than pursue charity status. When that email was received Ms Holt was just finalising her promised revisions to the documents submitted to her the previous day. She sent her revised document anyway at 1.28 pm. To meet the Fund launch date of May 16, the McCanns had obviously decided to abandon the apparently hopeful charity negotiations in order to meet the deadline for same day company incorporation. Documents must be filed by 3pm for the company to be incorporated on that day.

It is odd that the McCanns committed themselves to a launch date, set it would appear, before BWB were engaged. In an email to the Charity Commission, BWB refer to being instructed 'this afternoon' (i.e. Monday May 14). What difference would a couple of days delay have made? And it is clear from the documentation that the Charity Commission officials were helpful, and that it was likely that charity status could have been obtained with only minor delay with a little compromise by the McCanns.

Charity status is valuable because it gives an organisation credibility with the public, grant making bodies and local government, making it easier to obtain funds. It also gives the organisation tax advantages. Individuals, sole traders and companies can also benefit from giving to registered charities. Higher rate tax payers may be able to claim a tax refund. Under the Gift Aid scheme a donation is treated as if standard rate tax (20%) has been deducted and this is equivalent to an extra 25p in the £ for the charity. For donations between 6.4.2008 and 5.4.2011 the government gave an extra 3p in the £ supplement. Individuals can also have charitable donations deducted from their salaries, and this is tax efficient as their income tax is calculated on their salary after the donation. See www.hmrc.gov.uk/charities-donors/ for more information on the benefits to an organisation of charity status.

Charities must give an annual report and accounts to the Charity Commission and make these documents available to the public on request. There are also rules relating to fundraising. The trustees (directors) cannot normally receive salary, fees or contracts from the charity and nor can their spouses or other close family members. These requirements are not onerous or unreasonable. Having hired charity experts BWB on the advice of the paralegal, it is surprising that Kate did not let them have a day or two more to explore charity status. And it is surprising that the McCanns have not apparently revisited this issue.

In Chapter 9 in which Kate describes her activities of May 14 she does not mention any dealings with BWB who must have worked very hard that day. Nor does she mention dealing with the paralegal or anyone else at IFLG. There must have been urgent emails and phone calls that day from her advisors. She just states that charity status would not be forthcoming as it was deemed that the 'public benefit' test would not be met, and adds that it (the Fund) 'was set up with great care and due diligence by experts in their field.'

It would be more accurate to state it was set up with great haste and with no apparent reason for that haste.

Rather than going into detail about the busy day she must have had dealing with her lawyers, and why she made the decision to proceed with incorporation and abandon the negotiations for charity status, she talks of going for a run, her first since Madeleine went missing!

She mentions trying to focus on the imminent launch of Madeleine's fund but doesn't say when it was to be or explain why a limited company was required. A press launch can be called at short notice and given the high profile of the case at that time; it would have got a good media turnout however short the notice was. And again, it probably would not have been a problem to get another celebrity at short notice if the one booked to launch the Fund on May 16, Martin Johnson the rugby player, could not meet a rescheduled date.

And after they incorporated the company in 24 hours, BWB applied for British and European trade marks on 18 May 2007 and was given the reference 2456061. These trademarks protected fundraising, internet and print promotions. Again this action was unprecedented at this very early stage in a missing person case.

Review of the Memorandum of Association and Articles of Association filed in May 2007 reveals in 3.1.3 that one of the three objects of the company is to provide support, including financial assistance to Madeleine's family (my italics). Now this could mean uncles, aunts, parents and any blood relations.

This object was not included in the draft submitted to the Charity Commission on May 14. In fact the draft objects were different to the ones actually used for the company as incorporated. The objects in the draft were general, relating to missing persons and the education of the public and the promotion of sound administration of the law. An accompanying note from BWB headed 'proposed activities' did state that initially practically all the donations received would be used for the search for Madeleine, and that substantial funds would not be forthcoming if donations were not restricted in the first instance to her.

The objects of the company as incorporated are specific to Madeleine McCann, with a final object to pursue other cases when the objects relating to her case are fulfilled.

5.2.1 permits payments to directors as beneficiaries and 5.2.4 permits payment of rent where appropriate to directors for premises. Therefore, if the McCanns or family members used a room in their home to work for the Fund, the payment of rent from the Fund would be permitted if they should want it and the Board agreed.

The quorum for Board meetings is one third of the current Board membership. This makes the current quorum two, as there are now six directors. Three directors are family members. The Chairman has a casting vote. John McCann was Chairman until he resigned in July 2010. It is unclear who the current Chairman is. If Brian Kennedy (Kate McCann's uncle) - who was one of the original directors - took over as Chairman, then the McCann family has a majority at board meetings by virtue of the Chairman's casting vote.

The conflict of interest policy (Articles nos 37 and 38) is interesting.

It says (37.1) that directors with a personal interest in an upcoming vote must declare that interest, and (37.2) withdraw from the relevant part of the meeting, and (37.3) not be counted in the quorum for that part of the meeting relating to their personal interest and (37.4) have no vote on the issue affecting them. That is proper governance.

However no 38 states that 'no director shall be regarded as having a conflict of interest solely because he or she is also eligible to receive the support of the Foundation.'

A reasonable person would conclude there is a clear conflict of interest for a family member director if decisions are to be taken on payments of legal fees, rent for part of his/her private house for use as an 'office', and other costs not directly related to the search for Madeleine. The draft documents sent to the Charity Commission only contained no.37 so had those documents been adopted, the McCanns and family members would not have been able to attend or vote on issues regarding certain proposed payments to themselves.

Interestingly a revised Memorandum and Articles of Association was filed in Companies House in December 2011. This deleted the object to provide support including financial assistance to Madeleine's family. This particular object had attracted unfavourable comment in particular from internet bloggers. The motive for deleting this objective more than four years later is unclear. If the Board felt this minority criticism of the object was adversely affecting fundraising, it would presumably have changed it earlier.

On p.138 Kate says there needed to be independent people on the Board as well as John McCann, who is Gerry's brother, and her uncle Brian Kennedy, and at that time she had no idea how important these independent people would be when later there was 'massive scrutiny' of the Fund.

The composition of the Board varied during the first year. At the most there were nine directors meaning the quorum was three. Two were family members; three were friends – Esther McVey, Jon Corner and Dr Peter Hubner. It is not known whether Michael Linnett, a retired accountant based in Leicester or P J Tomlinson (who resigned on 28.12.2007) were friends of the McCanns. Friends can of course be very independent, but the optics of having a majority of family and friends on the Board is not desirable. Gerry and Kate became directors on November 12, 2008. Board numbers were reduced to six, following the resignations of Dr Hubner, Dr Skehan and John McCann in 2010.

Returning to the decision to set up a limited company, nowhere does Kate mention the more logical option of dealing with the donations coming in – to open a new bank account in Madeleine's name, or in the joint names of Madeleine and herself. Such an account could, if desired, have two signatures, her own and an independent signatory such as a solicitor or an accountant.

This could have been done quickly at no cost. Down the line, when the situation was clearer, another structure could have been considered.

In fact it is likely there already was a deposit account in Madeleine's name as many parents open up an account in their child's name as a place for depositing gifts from family and friends, and later to encourage the saving of pocket money. In addition, the Child Trust Fund scheme, introduced in September 2002 by the government and which provided a small amount to kick start these special accounts, could also mean there was an existing bank account in Madeleine's name.

Perhaps, the McCanns, who at the time of the meetings with the lawyers, must have been very distressed, meekly accepted the advice of the persuasive paralegal, and gave him the go-ahead. But the McCanns are clearly intelligent professionals and even given the sad situation, it is hard to understand why they accepted the advice.

The cost of getting a top legal firm to set up a limited company would surely have been of concern to them as the donations coming in were for finding Madeleine and not for lawyers. The legal pair would presumably have informed them of the ongoing compliance costs of operating a limited company such as the audit fee. The audit fees for the four years for which accounts are available total £31,585. You would have expected some comment from Kate in Chapter 9 after the lawyers had left, wondering if she was doing the right thing in spending the public's donations to set up a limited company.

The money already coming in would have been in cash, or cheques made out to the McCanns so there would have been no problem using the money to fund the search. By May 17 a bank account in the company name was open and, most surprisingly, auditors to the company had been appointed.

The Charity Commission in its FOI reply supplied a printout of the official Madeleine website (http://www.findmadeleine.com/) at 17 May 2007 giving information on the Fund including auditor details. Now the directors of a company appoint the auditors. At that date there were three directors, two family members John McCann and Brian Kennedy, and Gerry McCann's immediate boss Dr Doug Skehan. It is quite possible that IFLG or BWB recommended these auditors to the directors but that does not explain the rush to appoint them. It is normal for a company to meet with proposed auditors to agree exactly what they are to do (sometimes auditors may provide other services to the company), to agree fees and to draw up a letter of engagement. It is very unlikely in the time that any meeting with the auditors took place. The first meeting of the board according to Kate was due sometime in the week beginning May 20 which would appear to be the earliest time this non urgent matter could have been discussed.

The auditors appointed were haysmacintyre in London WC1, a 24 partner firm with 150 staff. It is perhaps surprising that the McCanns did not choose a local firm. It is usually more convenient to have a local firm and can be cheaper as a local firm normally has lower overheads than a central London firm. Keeping audit costs down means more money for the search so even though the firm haysmacintyre was possibly highly recommended by the lawyers, one would have thought that this decision did not need to be rushed. Auditing the accounts of a company like Madeleine's Fund would not particularly challenge any qualified person, so there would be no need to take on a large firm with special expertise.

Kate does not mention this firm in the book or the reason why they were chosen and why so quickly. Many new companies would not appoint auditors until later in the financial year though it is good practice to appoint at an early stage to have advice on setting up accounting systems with proper internal controls. But two days after incorporation is fast by any criteria. If an existing business decided to change its status to that of limited company then the accountants to the unincorporated business would normally become auditors to the limited company and would probably have set it up as part of their role. But this wasn’t the case here.

The official Madeleine McCann website says in the section about the Madeleine Fund:

'The majority of the fund money has been and continues to be spent on investigative work to help find Madeleine. Additionally money continues to be spent on the wider awareness campaign – reminding people that Madeleine is still missing and to remain vigilant. None of the directors have taken any money from the fund as remuneration.

Anyone who wishes further information with regards to the financial details of Madeleine's Fund and its professional advisors please refer to the accounts filed at Companies House.'

Kate says of the company on p.138 that 'from the outset everyone agreed that, despite the costs involved, it must be run to the highest standards of transparency.'

Fine words but the reality is different.

Looking at the information provided by the audited accounts as the website advises is interesting, but frustrating in the case of the years to March 31 2009, March 31 2010 and March 31 2011. The first accounts were made up from incorporation May 15 2007 to March 31 2008 and show an operating surplus of £1,031,065.

A page of analysis of expenditure was filed for the accounts to March 2008 which is not a statutory requirement but is good practice for such a company which is a 'not for profit company' according to the official website http://www.findmadeleine.com/.

I put the following question to the Press office at HMRC (Her Majesty Revenue & Customs)

'Has the term 'not for profit' any statutory meaning? It seems to be a catch all phrase used by organisations that may (or may not!) have very worthy aims and objectives.'

And the reply –

'It has no meaning for HMRC, only charities and CASCs (Community Amateur Sports Clubs) benefit from tax beneficial arrangements.'

So this term 'not for profit' which is widely used by companies/organisations that are not normal trading companies has no meaning for the UK tax authorities. While the term is generally used with no intention to mislead, it clearly is a term that should not automatically be taken at face value.

The additional page of expenditure information raised more questions than it answered. I put the questions and comments below to auditors haysmacintyre. When I raised these issues with the auditors, the March 2011 accounts were not yet available and hence the questions only relate to the accounts for 2008, 2009 and 2010.

To continue ...

Guest- Guest

Re: Madeleine's Fund: Leaving No Stone Unturned Limited - Forensic examination of the fund accounts by Enid O'Dowd FCA

![]() by Guest 11.01.23 19:57

by Guest 11.01.23 19:57

Continued ...

The auditors passed the questions to Clarence Mitchell, the McCanns official spokesman. I exchanged emails with him and finally received the following email:

I have now been authorised to issue the following brief statement from Madeleine's Fund in response to your approach:

"Madeleine's Fund - Leaving No Stone Unturned Limited" fulfils all of its legal requirements through the filing and public declaration of all the information that is legally required of it. It exists to support the search for Madeleine and remains entirely dedicated to finding her through everything that it does, fully in line with its published objectives."

I appreciate that this does not directly address your specific questions but this is all that the Fund wishes, or needs, to state at present. I hope it is helpful nonetheless.

Kind regards,

Clarence

So I am none the wiser, but more puzzled as to why the official spokesman is not facilitating what his clients claim they want – the ‘highest standards of transparency.'

In fact the official statement 'covers' three additional questions I put directly to Mr Mitchell.

Mr Mitchell referred me to Alison Barrow, at Transworld regarding the question about whether all book income is going to the Fund. I emailed her this question and also asked about sales to date in England and Ireland – but I only received a read receipt, and no subsequent reply.

I was surprised that Clarence Mitchell referred me to the publishers Transworld. Their obligation is to pay the contractual advance to their author. It is not their concern where the cheque ultimately ends up, and nor would they normally know.

I also addressed the questions below to BWB:

The FOI documents subsequently supplied by the Charity Commission partly answered these questions. As Kate has not said in the book or elsewhere that BWB acted pro bono or for a reduced fee, it is reasonable to assume they charged a commercial fee for the work they did under huge time pressure - a fee paid for by the many people who sent in money to help find Madeleine.

BWB sent me a brief emailed letter from partner Rosamund McCarthy on July 18 2011 referring me to Clarence Mitchell and saying that BWB 'no longer acts for the company.' However, a Current Appointments Report obtained from Company House on July 20, 2011 gave BWB Secretarial Ltd (the company secretarial wing of BWB) as the company secretary of the Fund. I asked Company House to clarify whether this was accurate in case a recent resignation had not been reflected in the Report – but was informed the Report was correct. I then raised this inconsistency with Ms McCarthy by email; I received a read receipt but no actual reply.

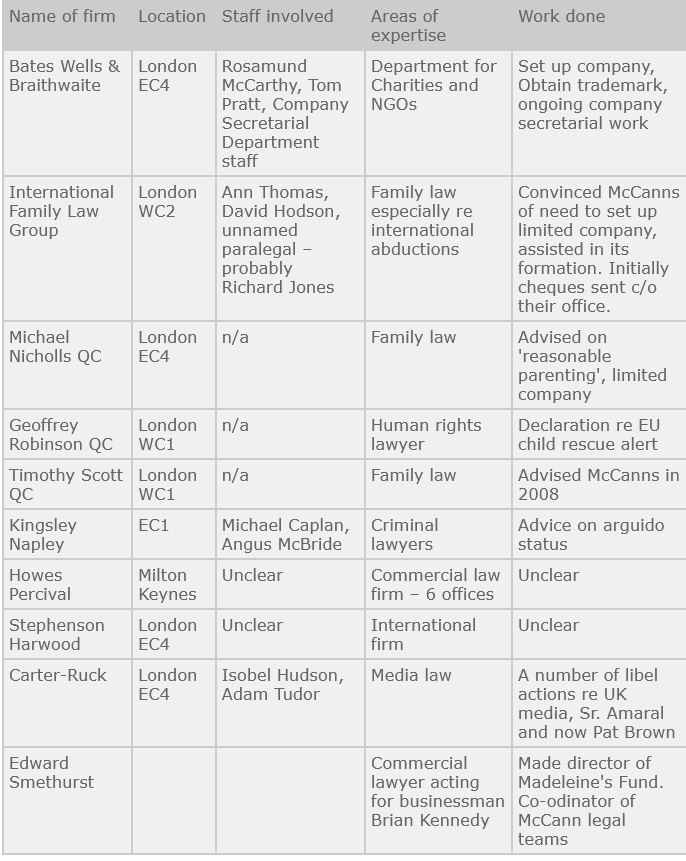

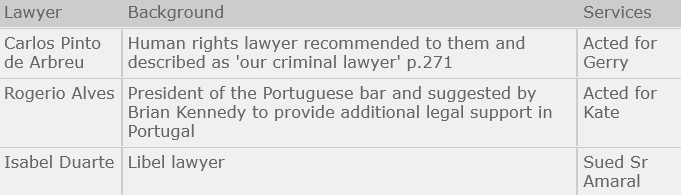

BWB are but one of a number of UK legal firms who have acted for the McCanns in the past four years, as the attached table shows. Limited company accounts normally contain a page of company information listing the company solicitors, bankers etc. For each of the four years for which accounts are available two firms of solicitors are listed. BWB are listed for each year including 2011 so presumably the date they parted company with the McCanns was after March 2011.

In the accounts for the period 15 May 2007 to 31 March 2008 the second named firm is Hayes Percival. This is a large firm with offices in 6 UK centres, but this firm is not mentioned in the book and it is unclear what legal services they provided. The accounts to March 2009, March 2010 and March 2011 name Stephenson Harwood, a large international firm with 100 partners, in addition to BWB. Other legal firms retained by the McCanns include Carter-Ruck, specialists in libel law and criminal law firm Kingsley Napley. Then there are the Portuguese lawyers.

How many other parents of missing children have needed so many lawyers?

The first lawyers retained were the IFLG and Kate has explained she met them as there was a connection with a colleague of Gerry's. But it's odd that they were retained given their expertise is in the area of family abductions resulting from marriage breakdown, a tricky area involving knowledge of family law in different countries. Madeleine's disappearance clearly wasn’t the result of a family abduction. If there was an abduction, then it was a straight forward criminal abduction with no legal issues once the police located the kidnapper. So why were the IFLG retained? According to the official website printout on May 17 2007, postal donations were to be sent c/o IFLG at their central London office.

Returning to the speed of setting up the company – while it is clear from the independent evidence of the Charity Commission that the process was started on May 14 and incorporation took place on May 15 – this was not the usual time span for a company being set up from scratch to the client's specification.

I contacted the Charities Section of BWB by email posing as a voluntary organisation that might need to incorporate quickly in connection with funding that would be dependent on incorporation, and which also needed charity status. I was quoted a fee of £3,500 – £5,000 and after an exchange of emails to tease out what was required, BWB agreed that while a timeline for speedy incorporation of Monday am (instructions taken) to Thursday (incorporation day) was possible, it would be better to allow a week.

Why did BWB agree to rush incorporation the way they did, given that a couple of days extra would not have in any way hampered the search for Madeleine? At that stage, the child could have been found at any time, dead or alive. Obviously their clients, the McCanns, instructed them to incorporate on May 15 because getting charity status was less important than not having to change the date of a press launch.

In the questions to the auditors I asked about the lack of expenditure detail after March 2008. There used to be information on donations in the early days of the official website. Now there is no financial information at all. Why not put up the audited accounts on the website? Is referring people to Companies House the transparency that Kate pledged?

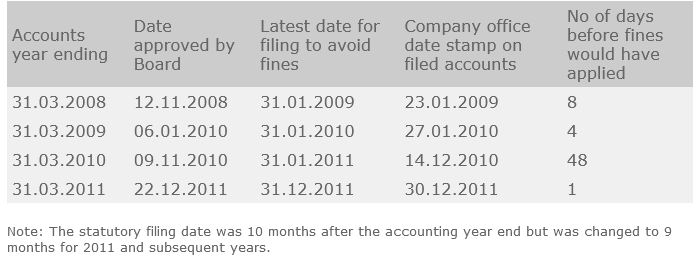

I noted that the accounts were always lodged close to the filing deadline. Why not file the accounts as soon after the balance sheet date as practical? Good practice demands early filing before the information becomes to some extent irrelevant. The Fund's accounts were filed as below:

Why was the equivalent expenditure schedule, filed relating to March 2008, not filed for March 2009, March 2010 and March 2011?

Clearly the directors decided to discontinue providing an analysis of expenditure in the filed accounts and instructed the auditors accordingly. A possible reason for the Board's decision is the public criticism that only 13% of expenditure appeared to go on searching for Madeleine in that year. That percentage may well have been inaccurate either way because the detail published in the filed accounts for 2008 in itself raised issues requiring further clarification. I could not get any clarification from the auditors or Clarence Mitchell so cannot throw any light on the accuracy or otherwise of the 13%.

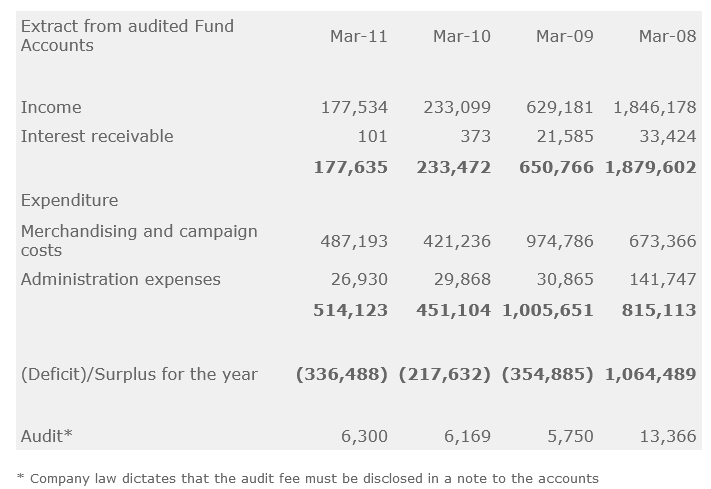

It is quite reasonable that an ordinary trading company would not reveal more information than legally required in its filed accounts because some information could be commercially sensitive and of use to a trade competitor. However, this argument would not apply to a company such as Madeleine's Fund where it would be to its advantage for the public to see where the money was going. But apart from 2008, the only information available on its income and expenditure from the filed Accounts is as below:

Another question I could not answer is the name of the 'experienced Fund Administrator appointed to ensure the highest standard of transparency and accountability' to quote the website. Clarence Mitchell would not disclose it, or rather it would appear his clients the McCanns, would not let him disclose it when I asked. It is common for company websites (whether normal trading companies or NGOs and charities) to give at least the name of their most senior person and his/her email address.

If the company had achieved charity status, the name of this person would have had to be revealed in the Annual Report that must be submitted to the Charity Commission. Reporting requirements for charities involve naming the CEO or other senior staff members to whom the day to day staff management is delegated by the trustees (directors).

And, as a charity, the accounts would have to be available to the public on request. As an ordinary limited company, a member of the public must know how to access the accounts at Company House and pay a small fee to obtain them.

Was Mr John McCann the Fund Administrator until he resigned from the Board in July 2010?

Both the Times (22.5.2007) and the Guardian (20.9.2007) reported that he was on indefinite leave of absence from his job as a medical representative with AstraZeneca. Other papers stated that he had actually resigned his job to look for his niece. The Guardian article said he had taken the leave 'to administrate the £1million fund.'

The official website states that 'none of the directors have taken any money from the fund as remuneration.'

But does that just mean money as payment for their work as directors specifically – or does it refer to all work they may have done for the Fund and for any services they provided which are unrelated to being a director?

If John McCann was the Fund Administrator or whether he fulfilled some other role for the Fund and did not receive payment from the Fund for his work, how did he meet his financial commitments? He returned to his company in the summer of 2010 after a three year break. It is unlikely that his company would have paid him while he was on this three year break. In general, career breaks for whatever reason, are not paid. According to his LinkedIn page Mr McCann left AstraZeneca in May 2011 for a position with Bayer.

The accounts for the year to March 2010 reveal in note 2 on p.8 that 'there were no employees in the year (2009 - none)'. This seems to contradict the statement in the Directors' Report for both 2009 and 2010 that the Fund 'provided some administrative support to Madeleine's family in maintaining the impetus of the investigation'. The March 2011 accounts do not have this note so we don't know if there were any employees or not in this year – though it appears from the Directors' Report that there was an employee because the Report states that the Fund has 'provided part-time administrative support to aid the investigation and campaign to find Madeleine (campaign co-ordinator and media liaison).'

'Curiouser and curiouser,' to quote from Alice in Wonderland.

The first year's accounts, where expenditure detail was filed, do not mention salaries; so it would appear there was no Fund Administrator or other employee unless he/she was paid by a benefactor outside of the Fund. However, there would be no reason to do this because this was the year with the biggest income, and the website had been (and still is) specific about hiring this most necessary employee.

And wasn't the whole point of using a company to have a formal structure through which all income and expenditure went?

Another indication that there were no employees is the apparent lack of an office. The company information given in the audited accounts gives the registered address as 2-6 Cannon Street, London EC4, which is the address of solicitors BWB. There is only a PO Box address in Leicester on the official website. In the 2008 accounts, where detail was provided, there is no item rent or rates under Administrative Expenses. For the subsequent years, as no expenditure breakdown is given we cannot know for sure, but as the note in the 2010 account states there were no employees for 2009 or 2010, there was no need of an office. If there was no office with the related costs of rates, heat and light, this raises the question as to what is included under Administrative Expenses in 2009, 2010 and 2011 other than the audit fee which we know as it has to be disclosed by law.

Could these 'other administrative costs' all relate to costs incurred by Kate McCann for using a room in her house for her work for the Fund. Clearly she would have costs like telephone, printer cartridges, postage, stationery and heating the room but these would hardly come to more than £20,000 pa? She might have to pay rates for the partial 'business use' of her house but even so, its hard to see how the administrative costs are so high in the context of this organisation. Costs relating to dispatching merchandise and campaign material would presumably be charged under Merchandising and Campaign costs and not under Administrative Expenses.

None of the four sets of accounts filed include any fixed assets. If there was an employee you would expect basic equipment for him or her: a desk and chair, a PC and printer and a filing cabinet.

Note 3 in the accounts for 2008 and 2009 shows a prepayment of £19,795 at both March 31 2008 and at March 31, 2009. Now prepayments normally relate to costs which have to be paid in advance like insurance, subscriptions or rent and rates. Most costs are paid when or after the goods or services are received. Now as it appears from earlier parts of this article that the Fund had no employees and no office, then employers' liability insurance, rent and rates would not apply. There could have been prepayments on a media monitoring subscription and possibly on a travel insurance policy relating to the directors who might be travelling abroad in connection with the search. However, any prepayments on such a subscription or on travel insurance could not possible equal almost £20,000!

For what could the Fund have paid such a substantial amount in advance? The major costs itemised in the 2008 accounts were legal fees and search fees. Could any of the companies involved have demanded significant money upfront as the audited accounts indicate? The Board would have had to agree to this. It is unwise to say the least to pay any company in advance for goods and services not received – unless there is a very good reason for doing so, perhaps because it is the only way to retain the services of a company essential to the aims of the organisation.

Examination of the accounts for the year ended 31 March 2011 lodged on December 30 2011, a day before the deadline for filing, throws up the question 'what happened to the advance for the book Madeleine which would have been paid in late 2010?'

The huge (unquantified) advance reported in the media in October 2010 does not appear to be in the accounts. If it was, it would either be included in the income figure in the Income and Expenditure Account or shown on the Balance Sheet with an accounting note to explain the payment had been received in the year and would be included in the Income and Expenditure Account for the year ending March 2012, the year in which the book was published. There is no balance sheet entry or note.

Could it be in the Income figure?

Unlikely as the accounts show total income of only £177,534 and no breakdown thereof. In this accounting year (year to March 2011) the official McCann website refers to four official fundraising events, three 'Bags of Hope' events - in the National Space Centre Leicester, in the Crypt in the Liverpool Metropolitan Cathedral and in the Crowne Plaza Hotel Glasgow - and an 81 mile sponsored cycle ride undertaken by Gerry, the Etape Caledonia, in Scotland. In addition to these official fundraisers there would presumably have been fundraising income from supporters around the country and profits from the sale of merchandise. Usually 'good causes' will indicate on their website or in their Annual Report or other publications how successful a fundraising event was. It might give the specific sum raised or alternatively indicate the kind of amount raised. The McCanns' website only gives basic information on the events held including where they were held. There is no mention of the amounts raised; the only comment is that the events were 'very positive.'

The Bags of Hope events featured an auction of donated bags, some from some very high profile celebrities. The Loughborough Echo (11.3.2011) said the three events hoped to raise 'tens of thousands of pounds.' Attendees, according to the News of the World (6.3.2011), paid £50 per head to attend. The venues used had substantial capacity. Kylie Minogue, Coleen Rooney, Fearne Cotton, Carol Vorderman, Chris Tarrant and Lorraine Kelly were among the celebrities who donated bags. Given the celebrities involved and the professional team behind the McCanns these events must have raised tens of thousands of pounds as the organisers hoped.

If the advance money is included in the income figure in the Income and Expenditure Account it must have been less than £100,000. Even allowing for media exaggeration about the advance, it is not credible that the Christopher Little Literary Agency who acted for Kate McCann would have accepted such an advance for a book that had such huge sales potential. This long established agency until recently acted for J K Rowling.

The other possible explanation, that there was no advance paid on signing the contract as is usual, is not credible either. No literary agent with a client with a 'hot' book would permit that.

So the likely explanation is that the advance was not paid into the Fund.

Its whereabouts is a mystery to me.

HMRC confirmed to me that there is no special income tax treatment for the income from writing a book, as for example there used to be in Ireland for certain writers and artists. Thus assuming the contract for the book was between Kate McCann and the publishers, then the money she received under that contract would be subject to income tax at current rates. The rates for the UK tax year 2010/2011 in which the initial advance on signing the contract would appear to have been received were : basic rate 20% applying to taxable income from zero to £37,400, higher rate 40% applying to taxable income from £37,401 - £150,000 and additional rate 50% on taxable income over £150,000. These income tax rates would take a sizable chunk of the advance, especially given that Dr Gerry McCann has a salary as a fulltime medical consultant and Kate's book earnings would attract income tax at 40% and 50%. Kate would need to file a tax return for 2010/2011 disclosing her book earnings (and any other earnings she might have had in that year) by 31 October 2011 if filing by hard copy, or by 31 January 2012 if filing online.

In addition to paying income tax on the book earnings Kate would have to pay commission to her literary agent. Her agent's website states that the agency's commission charge is 15%. Of course, a lower figure could have been negotiated as the book was to raise money for the search for Madeleine.

If the book contract was between the publishers and the Fund, then the advance clearly should be in the Fund accounts for the year to March 2011.

When I looked at the audited accounts to see what they said about taxation I found a note 1.3 Taxation as part of the Notes to the Financial Statements in accounts 2008, 2009 and 2010 which read:

'The company remains accountable for taxation liabilities arising from capital gains, interest, trading activities and any other surplus other than from donations received' (my italics).

In the accounts to 31 March 2008, there is a surplus of £1,064,489 before taxation but the corporation tax payable per the accounts is only £12,462. This is because most of the income for that period was from donations . According to the detailed schedule filed for this period - £1,390,360 donations were received through the bank and £391,740 donations were received via the website.

There is no note about taxation in the 2011 accounts, and I cannot understand why it has been removed. The taxation charge in the 2011 accounts is £8,371.

Another question I have about corporation tax arises from the 2010 accounts. The charge for corporation tax for the year in the Income and Expenditure Account is £2,598 but the figure for the corporation tax due in the analysis of creditors per the balance sheet (note 4) gives the corporation tax creditor as £4,666 rather than £2,598. However Note 3 which analyses the debtors figure on the balance sheet includes £2,068 'corporation tax debtor.' Deduct the corporation tax creditor from the corporation tax debtor and you have the corporation tax charge in the Income and Expenditure Account. The likely explanation of this is that the corporation tax debtor relates to a S.419 charge (ICTA 1988) on a director's loan not repaid within the prescribed time limits. In summary, where a director of a limited company takes a loan from the company and does not repay it within nine months of the end of the accounting period in which the loan was taken, a charge of 25% of the loan is payable to HMRC. This charge can be reclaimed when the director's loan is repaid. Thus it would appear that a director of the Fund took a loan of £8,272 from the company. Review of the 2011 accounts indicates that the director's loan had been repaid and that HMRC had repaid the £2,068 (25% x £8,272) to the company. For more information on S.419 see http://www.hmrc.gov.uk/ Corporation tax home page – 'Directors Loan Accounts and Corporation Tax explained.'

If there was a director's loan taken from the Fund, and obviously it would have been approved by the Board, it would be interesting to know the rationale for approving it because money, albeit temporarily, borrowed from the Fund reduces the funds available to search for Madeleine.

However, if there was a director's loan this would have to be included on the balance sheet as a debit, or the accounts wouldn't balance! Looking at the years involved, the balance sheets record 2008 – debtors total £585,369, 2009 debtors total £19,795 and 2010 – debtors total £3,718. In the notes to the accounts these totals are analysed except in the case of 2010. From the analysis the only place the 'loan' could be included is in the 'prepayments' £19,795 which has been queried earlier in this article. A director's loan is not a 'prepayment' but possibly has been misanalysed under this heading. If there was no director's loan then the corporation tax charge in 2010 is indeed a mystery.

As well as the taxation note changing, I see a change in Note 1.2 Income. The 2008, 2009 and 2010 accounts all state –

'Income comprises donations received by the company along with revenue recognised in respect of merchandise supplied, exclusive of VAT.'

But in the 2011 accounts the heading Income changes to Turnover and the note reads –

'Turnover comprises revenue recognised by the company in respect of goods and services supplied by the company, exclusive of Value Added Tax and trade discounts.'

Why has the word donations been deleted?

The website seeks donations and in interviews the McCanns always stress the need for money to continue their search. While donations to the Fund have obviously declined and the Directors' Report states this, there must have been some donations including money from small fund raising events held by the many supporters of the McCann family around the country.

Back to the 'missing' advance.

Of course you could argue that the book cover's promise of 'all royalties to the Fund' did not include the advance because this is a separate part of the payment for the book. However an advance is surely 'advance royalties' and should have been lodged to the Fund's bank account. It is pure semantics to argue that the advance is separate to the royalties, which would not be paid until after the book had been published and after the advance had been cleared by sales.

All the above makes me sceptical about Madeleine's Fund. Even the name is misleading because the usual connotation of Fund is that some charitable purpose is involved. The Fund or should I say the limited company is merely an ordinary private company filing the minimum accounting details to comply with the law, and filing close to the latest legal filing date.

The official website states that the Fund does not have charity status. Despite that, there is great public confusion as to the status of the Fund, which has not been helped by consistently sloppy journalism. As mentioned, the term 'not for profit' which is used by the company has no meaning to the HMRC, and given the lack of financial information, it is impossible to say whether the Fund would meet a reasonable person's interpretation of that term.

In the accounting year to March 31 2011, the McCanns lost two appeals in their case against Sr Amaral for his book 'The Truth of the Lie.' The Directors' Report does not mention this though it has financial implications for the company. In both the 2009 and 2010 Directors' Reports reference was made to paying for legal representation for the family in Portugal in connection with the Amaral case. Thus, it is reasonable to assume that these Portuguese legal costs were met in the year to March 2011 and will be met in the future. A further appeal by the McCanns is set for April 2012. Surely some mention of these ongoing legal costs should have been made in these accounts?

My final comment on the accounts is that the accounts for the year to 31 March 2009 have not been properly checked by the Board and by the auditors.

There was a DEFICIT for the year of £354,885.

Yet

•

The auditors report (p.5) refers to the SURPLUS for the year

•

The Income and Expenditure Account (p.6) consistently uses the word SURPLUS when the correct word is DEFICIT

•

In note 2 on p.8 the heading should be Operating Deficit and not Surplus and the text should use deficit and not surplus

•

In note 3 on p.8 the comparative year should read 2008 and not 2009

Director Brian Kennedy (Kate's uncle) approved these accounts on behalf of the Board on 6.1.2010 and signed them on p.7. The auditors then filed these accounts at Companies House.

On July 14 2011 I emailed the Find Madeleine campaign (using another name) suggesting that financial information including the audited accounts be put on the website. I also referred to difficulties ordering a holiday pack. On July 18 I received an email from 'Karen' telling me the accounts were available in Companies House and that she would pass my suggestion 'on to the team and see what they think.' She said there had been difficulties with the online ordering store and I could order via the general email while the problem was being solved. There was no follow up email telling me what the team thought of my suggestion and no change in the lack of financial information on the website!

After reviewing the background to the setting up of the Fund and its published accounts, and getting such information from independent sources as was available, as a chartered accountant who has also worked both in a paid and voluntary capacity for charities and for 'not for profit' organisations, I am unable to understand why in the context of a missing child -

•

the Fund (limited company) was set up only days after Madeleine vanished

•

the accounts, apart from 2008, are so uninformative

•

what has happened to the advance for the book Madeleine which does not appear to have been put into the Fund as people expected

•

whether the Fund ever had any paid staff and in particular whether there ever was a Fund Administrator as the official Madeleine website states

•

the reluctance to provide meaningful financial information

•

the need for so many professional advisors, mainly lawyers and whether their fees were paid fully or in part from the Fund

•

why the issue of charity status has apparently not been revisited given the obvious benefits to the search for Madeleine

People everywhere have been touched by the story of this missing child. Many have sent in money they could perhaps ill afford. These people deserve to be treated with respect; and that means publishing detailed and up-to-date information as to what the money has been spent on.

Respect also means answering reasonable questions from the press or from the general public. My observations are based on the evidence available and my professional experience. If some observations are a little wide of the mark it is due to the lack of transparency I have experienced. Some genuine transparency from the McCanns and their advisors would hopefully sort out my concerns.

I quote again what Kate says in her book on p.138:

'From the outset, everyone agreed that, despite the costs involved, it (the Fund) must be run to the highest standards of transparency.'

You would think that with the PR expertise at the McCanns' disposal, this would be the case.

It is not.

Why?

Enid O'Dowd February 2012

Enid O'Dowd February 2012

Note: the numerical references to the Memorandum and Articles of Association quoted in this report relate to the documents filed on 15 May 2007.

Accounts period to March 31, 2008

Campaign Management £123,573

What exactly does this cover? Does it include, for example, fees paid for PR services? If it does, is this for all PR services or only those that relate to promoting the Fund as opposed to dealing with media comment critical of the McCanns?

Legal Fees

A total of £180,321 has been paid (£111,522 under Merchandising and Campaign costs and £68,799 under Fund legal fees).

The cost of setting up the limited company (which did not involve acquiring charity status) could not have been more than £5,000 leaving £175,321 spent on other legal services.

What legal activities did this expenditure cover?